Nvidia Worth $22 Trillion? This Old-School Financial Model Says Yes.

Nvidia shares should be worth a lot more than they are now—400% more, to be exact. And most software stocks should be worth less—some a lot less—than they are now. You can find assessments like these all over social media, but in this case, they come from one of the most respected quantitative investing models in finance.

UBS HOLT is that model, and it has rarely loved a stock as much as it does Nvidia’s. “We think share price should be 400% higher,” said John Talbott, the U.S. head of HOLT’s technology coverage. That would put Nvidia’s market capitalization at a mere $22 trillion (compared with $4.46 trillion on Wednesday morning). It’s a big number for investors to swallow. “That’s the big pushback I get,” he said.

Talbott is less optimistic about the future of software. Viewed through the HOLT lens, software companies are generally expensive relative to their expected future growth rates. The market generally agrees, the industry lost $2 trillion in market value this year, but HOLT provides a smart framework for understanding software companies and picking potential winners. One winner could be Adobe, whose battered share price implies zero future growth. In this case, the market might be too negative.

Serious financial analysts have used UBS HOLT for decades because it strips companies down to one critical metric—how much cash they earn on the money they invest in their business. It doesn’t matter whether the company makes semiconductor chips, car tires or hamburgers—the metric is the same: cash flow return on investment.

CFROI, HOLT argues, improves on commonly used metrics such as return on equity and return on invested capital by stripping out accounting distortions, emphasizing cash flow and adjusting for inflation. It then combines CFROI with the company’s assets and its current and future growth to measure what it’s worth.

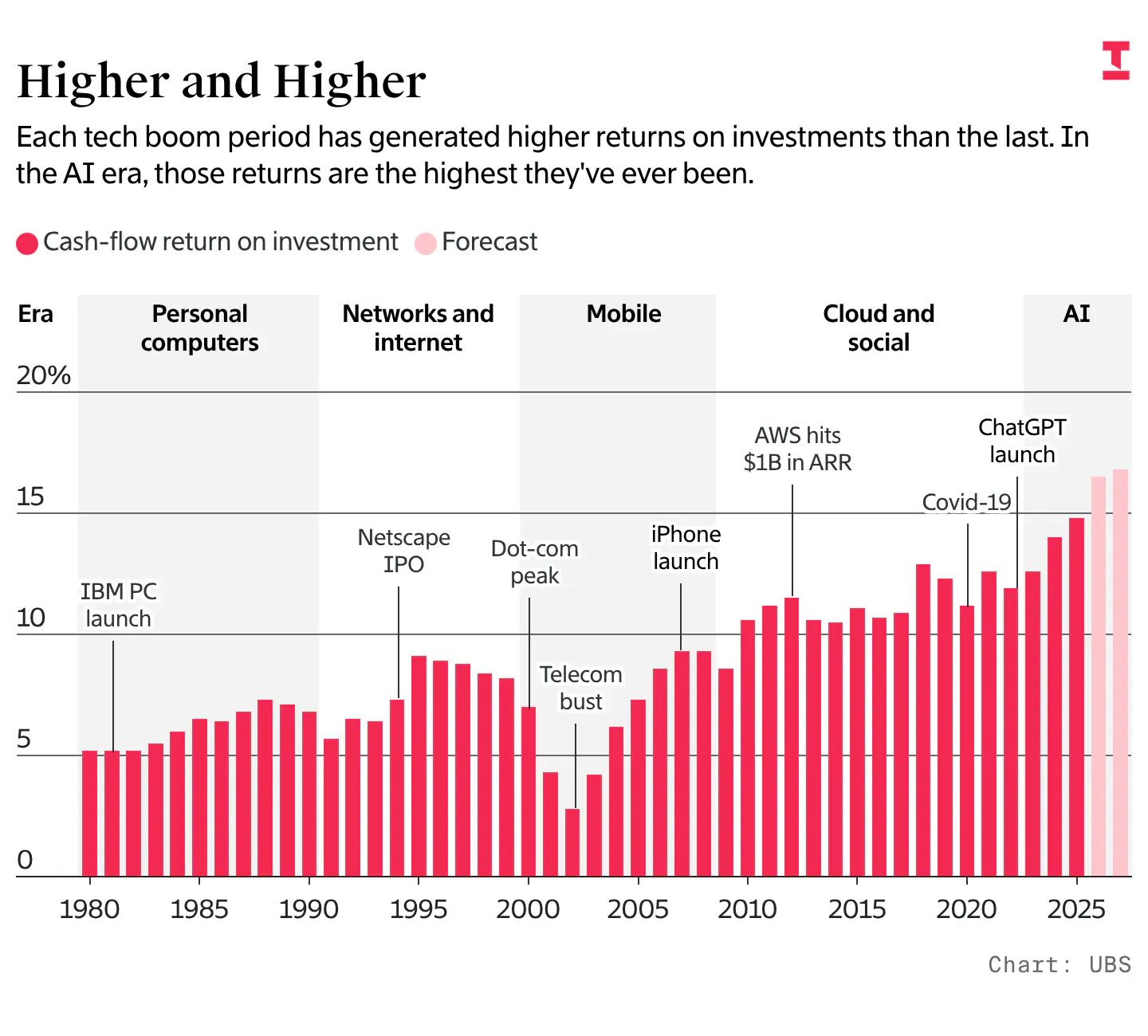

The model is well suited for analyzing tech. One reason is that it assumes every company’s growth rate will fade over time, even Nvidia’s. Every company’s CFROI will also decline until it is in line with that of the average company. HOLT believers will happily show how the model predicted fading growth for Yahoo, Cisco and Sun Microsystems during the dot-com bubble.

“There comes a time in every tech cycle when today’s winners are not the winners of the future,” said Talbott, who has been a HOLT analyst for nearly 17 years.

The HOLT model dates back to the 1970s, and the company formed in 1985. Credit Suisse bought it in 2002, and when that bank failed, HOLT landed at UBS. Its 550 clients range from mutual fund managers to sovereign wealth funds. HOLT tracks 20,000 stocks globally.

Why is HOLT so infatuated with Nvidia? The chip company has delivered some of the best long-term performance ever registered on HOLT’s metrics. The CFROI for the average nonfinancial company is 6%, but Nvidia is at 73%, putting it in the top 0.1% of all companies. And Nvidia’s asset growth, using typical balance sheet numbers such as capital expenditures plus other metrics, is in the top 0.5% of companies. “We’ve never seen anything like this in our system—it’s incredible,” Talbott said.

Just as important, Nvidia has beaten the fade. Its returns have continued to rise when HOLT’s model predicted they would fall. Nvidia has also focused on growth, which is exactly what a company with such a level of return should do in HOLT’s model. Companies with weak returns should focus on improving profitability rather than growth, HOLT advises.

HOLT doesn’t issue buy and sell recommendations, and its model better suits broad investment themes rather than individual stocks. But the model offers insights investors might otherwise miss, and it lets its clients plug in their own variables—say, for sales growth—if they think its assumptions are wrong. Analysts looking at Nvidia could, for example, account for the circular financing deals the chipmaker has done with its customers.

Software is one industry where HOLT stands out, not because of its stock predictions but because the firm is obsessed with the cash companies generate and with making data comparable across the entire market.

That’s important for software, where stock-based compensation, such as employee stock options and restricted stock, is far higher than it is for the market overall. At companies such as Palantir and CrowdStrike, stock-based compensation equals more than 20% of sales, according to HOLT.

Stock-based compensation is deducted from official earnings but many companies try to get investors to look at disclosures that ignore it. Companies often don’t include stock-based compensation when they give earnings guidance. That makes it hard to make comparisons across the industry.

HOLT sees stock-based compensation as an economic cost and deducts that figure from current and projected cash flows. It considers options that can be exercised as debt.

By making all of the numbers comparable, HOLT’s model helps make sense of an industry in turmoil. It would be easy to say the sell-off in software companies has made some of the stocks cheap. Most of the industry is still growing sales and generating CFROIs above 20%, far higher than the overall market.

However, HOLT shows the impact of stock-based compensation on the companies’ results, oftentimes making them look less impressive. It also invokes the fade, assuming that the industry’s historic high growth rates won’t last. “The trillion-dollar question is, are we not fading it enough?” said Talbott.

Combining company fundamentals with market expectations can yield interesting results. HOLT says among large software companies, only Adobe is priced for zero sales growth, while Oracle, Microsoft, Salesforce and Intuit are the only ones investors believe will grow less than 5%. Deep pessimism often precedes good returns.

Nvidia and the software makers are in some ways the bull and bear cases for AI. If Nvidia keeps crushing it, today’s software growth numbers might in retrospect sound ridiculously optimistic.

New From Our Reporters